EU tobacco taxation rests on invisible evidence – FISC is pushing a proposal that cannot withstand daylight

02nd Apr 2026

Negotiations on the EU’s new Tobacco Taxation Directive (TTD) have stalled. Officially, the disagreement concerns technical details and institutional processes. In practice, a far more serious question is emerging: who is actually scrutinising the evidence behind one of the EU’s most far-reaching tax proposals?

FISC’s role and influence

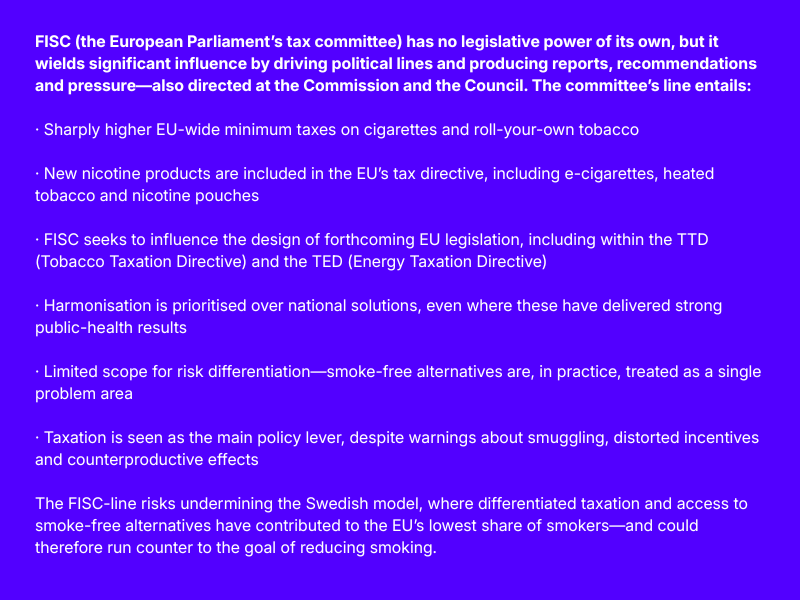

The European Parliament’s tax committee, FISC, is pushing for sharply higher and harmonised minimum taxes on all tobacco and nicotine products, including smoke-free alternatives such as nicotine pouches. The committee has no legislative power of its own, but it wields significant influence by driving political lines and through reports, recommendations and pressure—also directed at the Commission and the Council. In this way, it seeks to shape EU legislation, including within the TTD and the TED.

An evidence base kept behind closed doors

At the same time, lawyers and observers are now questioning why the underlying basis for the reform has not been made available for external review. The economic models that are supposed to show effects on consumption, tax revenues and illicit trade are still being kept behind closed doors.

This is no mere formality. When the EU requires Member States to rewrite their tax systems, decisions must rest on open, verifiable and proportionate analysis. Instead, the FISC line is built on what has been described as an “invisible evidence base”—something that risks undermining the legitimacy of the entire reform.

“This is no longer just about tax policy. When the EU refuses to show which calculations and assumptions are steering the proposal, it becomes a democratic problem,” says Markus Lindblad, Head of External Affairs at Pouch Patrol.

Harmonisation over harm reduction

At the same time, the FISC proposal is marked by a clear political ambition. New nicotine products are to be taxed at EU level to avoid differences between Member States—even when those differences reflect well-functioning national solutions.

Sweden is the clearest example. With the EU’s lowest share of smokers, the country has shown that differentiated taxation—where smoke-free alternatives are more accessible than cigarettes—can deliver real public-health gains. Yet that experience is given no meaningful space in FISC’s work.

“Sweden is being punished for succeeding. Instead of learning from a country that has reduced smoking fastest in the EU, they choose to dismantle the model,” says Lindblad.

Modelling that ignores behaviour

The FISC proposal relies heavily on models that calculate prices and revenues, but it overlooks how people actually behave. When smoke-free alternatives are taxed heavily, the incentives to switch away from cigarettes weaken.

“The EU says it wants to reduce smoking, but it is now pursuing a policy that risks locking people into cigarettes. That is both cynical and dangerous,” Lindblad notes.

A choice for the EU

The EU faces a choice. Either it continues to push a tax proposal whose basis cannot be scrutinised, where risk differences are ignored and well-functioning national models are sacrificed for uniformity—or it chooses transparency, evidence, and policies that actually save lives.

Right now, FISC is pointing in the wrong direction.